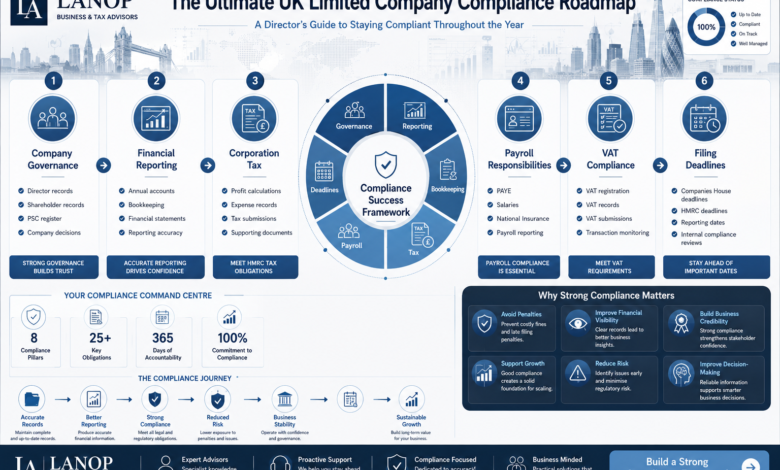

The Compliance Tasks Every UK Limited Company Cannot Afford to Ignore

Most directors think they’re on top of it. The accounts get filed, the tax gets paid, and the accountant sends a reminder every so often. Then one morning, a Companies House notice lands in the inbox or worse, a penalty charge from HMRC and the uncomfortable truth surfaces: statutory compliance services exist precisely because compliance is not as automatic as most people assume.

The risks are not abstract. Late annual accounts attract automatic fines that escalate the longer they sit outstanding. A missed Confirmation Statement can trigger a Companies House strike-off process, which means the company ceases to exist. HMRC interest charges accumulate quietly on unpaid Corporation Tax. And director liability, a concept many business owners consider theoretical, becomes very real the moment enforcement action begins.

This guide covers every statutory obligation a UK limited company carries throughout the year, in plain terms that make the responsibilities clear, the deadlines visible, and the consequences of missing them impossible to ignore.

What Statutory Compliance Actually Means?

Statutory compliance means meeting the legal obligations that exist because your company is incorporated. When you register a limited company at Companies House, you take on a set of duties that sit completely separately from running the business itself. Winning clients, managing cash flow, hiring staff that is the business. Filing accounts, submitting tax returns, maintaining statutory registers that are compliance. Both are non-negotiable, but only one comes with automatic penalties if you fall behind.

The obligations cover two main areas: what you report to Companies House and what you report to HMRC. Every limited company, whether it turns over ten million pounds or sits dormant with no trading activity, carries these responsibilities from the day it is incorporated.

Is It the Company’s Responsibility or the Director’s?

This is where a lot of directors get comfortable in the wrong way. The legal responsibility for ensuring a company meets its filing obligations sits with the directors, not the company itself. Hiring an accountant shifts the practical workload; it does not shift the legal accountability. If a return is filed late, HMRC does not pursue the accountant. The penalty goes to the company, and in serious cases, enforcement action falls on the directors personally.

Companies House vs HMRC: Two Authorities, Two Completely Different Jobs

Confusing Companies House with HMRC is one of the most common mistakes directors make, and it leads to genuine filing errors. They are entirely separate organisations with entirely separate requirements. Filing with one satisfies no obligation to the other.

| Companies House | HMRC |

| Annual Accounts | Corporation Tax Return (CT600) |

| Confirmation Statement | Corporation Tax Payment |

| Director & PSC Updates | PAYE / Payroll |

| Registered Office Changes | VAT Returns |

Companies House is a public registry. Its job is to maintain accurate records about every incorporated company in the UK and make those records publicly visible. HMRC is the tax authority.its job is to collect the right amount of tax. Missing a deadline with Companies House puts the company’s existence at risk. Missing an HMRC deadline costs you in penalties and interest. Both matter enormously, and they operate on entirely different calendars.

The Core Filing Obligations Every Director Must Know

Starting with Companies House, every limited company must file annual accounts once a year. For a private limited company, the deadline is nine months after the end of the accounting period. A company with a 31 March year-end has until 31 December. New companies get slightly longer for their first set of accounts twenty-one months from incorporation but that window closes faster than most expect.

The Confirmation Statement is a separate obligation that trips up a surprising number of directors. It is not a financial document. It simply confirms that the information Companies House holds about your company registered office, directors, shareholders, PSC details is still accurate. It costs £13 to file online, takes about ten minutes, and must be submitted within fourteen days of the annual review date. Missing it starts strike-off proceedings. That is a wildly disproportionate consequence for a ten-minute task, but the rule stands.

On the HMRC side, Corporation Tax is where the most common confusion arises specifically around the difference between when the tax must be paid and when the return must be filed. The payment is due nine months and one day after the accounting period ends. The CT600 return is due twelve months after the period ends. A company with a 31 March year-end owes its tax payment by 1 January, but has until 31 March to file the return. Directors who confuse these two dates and many do end up paying interest on late tax even though they filed on time.

VAT registration becomes compulsory once taxable turnover exceeds £90,000 in any rolling twelve-month period. Once registered, most businesses file quarterly returns through HMRC’s Making Tax Digital system. Paper returns are no longer accepted. Every return is due one month and seven days after the end of the VAT period, and missing that deadline triggers surcharges that increase with each repeat offence.

PAYE applies from the moment a company takes on an employee, including a director drawing a salary. Real Time Information means a Full Payment Submission must reach HMRC on or before every single pay date,there is no monthly catch-up. Missing even one submission generates a penalty, and the fines accumulate quickly across multiple pay periods.

The Annual Accounts Penalty Structure

Late filing penalties from Companies House are automatic. There is no grace period, no discretion at the lower end, and no option to appeal on the grounds that you simply forgot. The fines begin the day after the deadline passes and escalate based on how late the accounts arrive.

| How Late? | Penalty (Private Company) |

| Up to 1 month | £150 |

| 1 to 3 months | £375 |

| 3 to 6 months | £750 |

| More than 6 months | £1,500 |

| Second consecutive late filing | Penalty doubles |

Beyond the financial penalties, persistent non-filing leads to strike-off action. Companies House issues a notice, waits a period, and dissolves the company. Once struck off, the company’s assets vest in the Crown. Getting the company restored requires a court application that costs significantly more than any filing penalty would have.

The Obligations Most Directors Overlook

The big filings accounts, tax returns, VAT tend to get done because they come with obvious deadlines and obvious penalties. The requirements below cause just as many problems, but they slip under the radar because they are event-triggered rather than calendar-triggered.

A director who leaves or joins Companies House must be notified within fourteen days. Shares transfer from one shareholder to another the register of members must be updated and Companies House informed. A PSC’s details change fourteen days to report it, and failure is a criminal offence, not merely a civil penalty. The registered office moves fourteen days again, and any legal notices sent to the old address are still considered validly served.

Every limited company must also maintain a set of statutory registers: a register of directors, a register of members, and a register of Persons of Significant Control. These are kept by the company, not filed with Companies House, but they must be accurate and available for inspection if requested. Letting them fall out of date is one of the most common compliance failures precisely because nobody sends a reminder.

Director identity verification is another requirement that many have not yet addressed. Under the Economic Crime and Corporate Transparency Act 2023, all directors must verify their identity with Companies House through the GOV.UK One Login system or via an authorised professional. New directors must verify before appointment. Existing directors are working through a transitional period. Once Companies House enforces this fully, unverified directors will find their ability to make any filings restricted which is a significant operational problem.

Dormant Companies Are Not Exempt

A company that stopped trading three years ago still needs a Confirmation Statement and dormant accounts filed every year. Many directors forget this entirely until Companies House sends a strike-off notice. The filing burden is lighter than for an active company, but it does not disappear. HMRC also needs to be notified of dormant status. Treating an inactive company as invisible is one of the most avoidable reasons directors end up in strike-off proceedings.

What Happens When Deadlines Are Missed?

Missing the Confirmation Statement starts strike-off proceedings with no direct financial fine; the consequence is potentially losing the company itself. Missing annual accounts brings automatic monetary penalties that double on a second consecutive failure. A late Corporation Tax return triggers an immediate £100 penalty, rising to £200 beyond three months, with further tax-related penalties applied at eighteen months. Late VAT returns attract surcharges that increase in rate with each repeat offence. Late PAYE submissions generate per-submission penalties that stack up painfully across multiple pay runs.

The pattern across all of these is the same: the first missed deadline is costly. The second is considerably worse. And the further things drift, the harder and more expensive it becomes to catch up.

A Quick Compliance Health Check

Run through these questions quarterly. Any answer of “not sure” is the gap that eventually leads to a penalty.

Have annual accounts been filed on time for the last two years? Has the Confirmation Statement been submitted within the last twelve months? Is Corporation Tax up to date both the return and the payment? Are all VAT returns filed and payments current? Are PAYE and RTI submissions up to date for every pay period? Have all changes to directors, shareholders, and PSCs been reported to Companies House within fourteen days of happening? Is the registered office address current on the public register? Are statutory registers held, accurate, and up to date? Have all directors completed identity verification?

The quickest external check is to search your company name on the Companies House public register. It shows when accounts and Confirmation Statements are due and flags anything already overdue.

How Professional Support Changes the Picture?

A single-director company with no employees has a manageable compliance footprint. Add staff and PAYE becomes a permanent part of the calendar. Cross the VAT threshold and quarterly MTD filings follow. Bring in a second director or issue shares to an investor and the registers need updating immediately. None of these changes are individually complicated; together they create a web of overlapping deadlines that grows genuinely difficult to manage from memory alone.

Growth also changes the risk profile. A small company that pays a late filing penalty is embarrassed. A company turning over several million with incomplete payroll records or an HMRC enquiry triggered by a CT600 discrepancy faces a very different problem.

This is where statutory compliance services make a structural difference not as a luxury, but as a process. A professional compliance service maintains a rolling picture of every obligation, monitors deadlines, flags changes in law, and ensures that when something changes inside the business, the reporting keeps pace with it. The companies that stay consistently compliant are not necessarily run by directors who know every regulation inside out. They are run by directors who know which responsibilities require a proper system behind them.

Frequently Asked Questions

What is the difference between Companies House and HMRC obligations?

They are two separate authorities with two separate sets of requirements. Companies House wants your annual accounts, Confirmation Statement, and director updates. HMRC wants your Corporation Tax return, VAT returns, and PAYE submissions. Filing with one satisfies nothing with the other, and missing a deadline with either carries its own consequences.

Does a dormant company still have compliance obligations?

Yes. A dormant company still needs a Confirmation Statement and dormant accounts filed every year. HMRC also needs to be notified of dormant status. The filing burden is lighter than for an active company, but it never disappears. Assuming an inactive company needs no attention is how directors end up with a strike-off notice.

Can a director be personally liable for missed compliance deadlines?

In most cases penalties fall on the company. However, where PAYE has been deliberately avoided, fraud is involved, or a director has seriously breached their legal duties, personal liability becomes very real. Director disqualification is also possible. Having an accountant handle the filings provides no legal protection the duty sits with the director.

What happens if a Confirmation Statement is not filed?

There is no direct monetary fine, but Companies House will begin strike-off proceedings. If the statement remains outstanding, the company is dissolved and its assets vest in the Crown. Restoring a struck-off company requires a court application that costs far more than the £13 filing fee ever would have.

How often should a director review the company’s compliance position?

At minimum, once a quarter. Calendar-based obligations like accounts and VAT returns can be mapped out at the start of the year. Event-triggered obligations: a new director, a share transfer, a PSC change carry a fourteen-day reporting window that starts the moment the change happens. Treating every internal change as an immediate compliance trigger is what keeps a company consistently clean.

Conclusion

Most compliance penalties happen because someone assumed a deadline was further away than it was, or trusted that someone else had handled it without checking. The obligations are finite and learnable; the real risk comes from letting things drift.

Build deadlines into your own calendar. Treat every internal change as a compliance trigger the moment it happens. And when business growth makes it difficult to keep a clear picture, that is when professional support becomes a necessity.

Lanop Business & Tax Advisors helps UK limited companies stay on top of every statutory obligation from annual accounts and Corporation Tax to PAYE and company record updates so nothing gets missed and directors can focus on growth.

Ready to get compliant and stay that way? Speak to a tax advisor London businesses trust. Lanop Business & Tax Advisors is here to help.